In this analysis, I’m taking a look at an idea for making the Anchor yield reserve self-sustainable. Here’s the idea:

Post Columbus-5 upgrade, all of the seigniorage is being burnt. What if a part of this seigniorage can be captured to bolster the Anchor yield reserve?

But first…

What Is Seigniorage?

For the traditional definition of the term, I’ll let Investopedia’s crack SEO team explain because they rank #1 on Google for “seigniorage” SERP.

Seigniorage is the difference between the face value of money, such as a $10 bill or a quarter coin, and the cost to produce it. In other words, the economic cost of producing a currency within a given economy or country is lower than the actual exchange value, which generally accrues to governments who mint the money.

If the seigniorage is positive, the government will make an economic profit; while a negative seigniorage will result in an economic loss.

In terms of Terra, Do explains what seigniorage is here

For more info on the term, check out the below 2018 big brain post from Do 🧠

And if you’re still confused, then read this redditor’s post where they have finally discovered the meaning of life…errr…seigniorage 🤌

Data Analysis

Ok, so with the opening act out of the way let’s get to why ya’ll are here.

Here are the ground rules:

- I’m only looking at the data post Columbus 5 upgrade i.e. After September 29, 2021

- UST and LUNA can both be burnt to mint the other asset and could be considered seigniorage. But in Do’s explanation above and Terra docs, I’ve only seen LUNA burnt being called as seigniorage. So, in my seigniorage calculations, I’m only including LUNA→UST burn/mint route.

- The seigniorage conversion from LUNA to $USD prices used the average price of LUNA on the day seigniorage was produced.

With that out of the way, let’s look at some data!

First up, let’s get a sense of how much net LUNA’s been burning daily. The wizard from Hogwarts has been posting up and down CT about 1M+ LUNA burn days and it checks out here. Almost the entire month of March was a 1M+ LUNA burn kind of month.

CryptoHarry was right! Take that Professor Snape!

Historical Rollback

In this part of the analysis, I’m look at what would’ve happened if we had implemented the seigniorage redirection proposal with Columbus-5 upgrade.

Weekly Seigniorage Generated

First, we convert this burnt LUNA to the total amount of seigniorage in $USD terms (assuming this would have been captured by the protocol). In $USD value, we’re generating more than $200 million seigniorage almost every week and in some weeks as high as ~$1B.

So, what happens when we start redirecting (read: capturing instead of burning) some of this seigniorage?

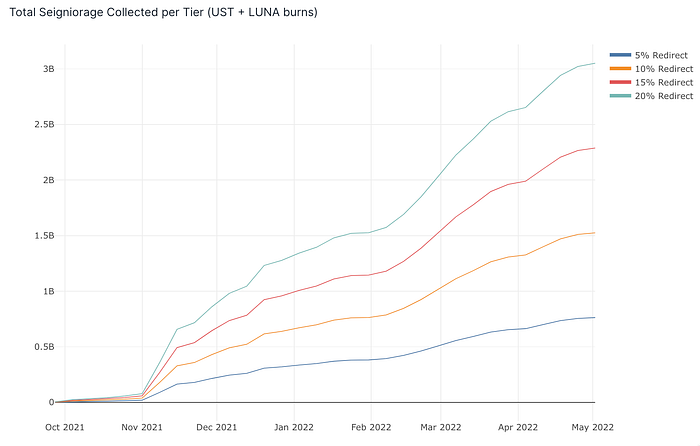

Cumulative Seigniorage

Well, we can model this out post-Col 5 when this burning of the seigniorage started. If we had captured various percentage of seigniorage, based on different rate of capture, we’d have the following amount of seigniorage accumulated:

- 5% redirect — $800M

- 10% redirect — $1.5B

- 15% redirect — $2.3B

- 20% redirect — $3B

Wooo! That’s a lot of seigniorage that we burnt there.

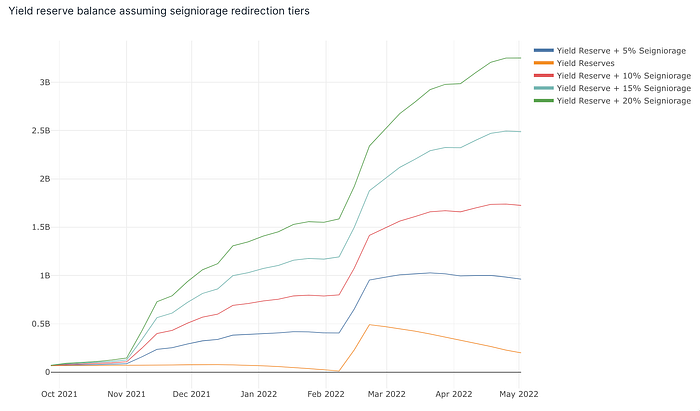

Redirected Amount + Yield Reserve

Now, let’s assume we had redirected those amounts to the Anchor yield reserve to see what kind of an impact it would’ve had.

How to read the below chart: I’m taking the daily historical yield reserve balance and adding the seigniorage amounts obtained from the above seigniorage captured tiers.

- Immediately we can see that the yield reserve (yellow line) isn’t looking healthy all by itself and is starting to deplete again with only a few weeks remaining.

- If we had redirected even 5% of the seigniorage, we would be sitting in a lot better place now. The yield reserve would be at $1B and decreasing at a much slower rate.

- For higher tiers (10%, 15% and 20%), we would be increasing the yield reserve each week even at the current Anchor Earn demand.

Future Projections

Now, let’s look into the future to see how this model continues.

UST Minted

First up, we need to figure out how much UST is going be continued to be minted every week. Based on the past data, I came up with the following rough estimate of mints per week that puts us at around $26 Billion market cap by beginning of October.

NOTE: How I came up with the future UST minted?

Listen, I’m no statistician. I’m just a guy who knows how to write some SQL and turn the output into some pretty pictures. So, I did what any guy in my place would do.

I searched for “forecasting algorithm” on google.

This returned me a list of various forecasting functions in the tool underpinning the entire global financial industry — Microsoft Excel

Then, I used the FORECAST.ETS function which uses something called AAA version of the Exponential Smoothing (ETS) algorithm and let it run on past 8 months of UST mint data.

Yeah.

No idea about the details of how that ETS function works but we don’t need to (yet). I played around with a few parameters until the prediction didn’t look wack.

So there you have it folks, that’s how I minted UST into the future.

(Something something about 90% of the statistics are made up including this one)

If you have a better idea then…….don’t @ me. If you’re a statistician, you can probably model this better and I’m happy to learn.

Yield Reserve Balance

Next, I looked at the rate of depletion of yield reserve and came up with three growth scenarios where the yield reserve runs a deficit in the future without any external help or top-up from TFL. I projected the following deficits for the yield reserve based on different growth rates for Anchor Earn deposits.

- Slowing Anchor Earn growth rate — $(275M)

- Current Anchor Earn growth rate — $(440M)

- Increased Anchor Earn growth rate — $(720M)

Now, if we redirect 5% of the seigniorage to the yield reserve, here’s where we end up in the three Anchor Earn deposits growth scenarios.

- Current growth rate — the yield reserve decreases at a slower rate

- Faster growth rate — the yield reserve shows a similar rate of decrease to the current model of no seigniorage redirection.

- Slower growth rate — The yield reserve actually starts increasing.

Closing Commentary

Redirecting the seigniorage to the Anchor Earn seems like one of the best ideas I’ve heard about making the Anchor Earn side self-sustainable. In this analysis, I’ve shown three growth projections and how the various tiers of seigniorage will help.

It’s likely that if the 20% APY continues to be provided, then it’ll attract even more deposits (I’ve heard some startups are putting their seed money into Anchor Earn 🤯). Therefore, the “Faster growth” scenario is likely to play out. This means that the community governance will need to decide which seigniorage capture tier needs to be implemented. The seigniorage capture tier can always be adjusted based on Anchor Earn demand as well.